Repeat Adverse ICFR Assessments

Subscriber Content

Preview Image

Image

Effective Strategies for Managing Repeat Adverse ICFR Assessments

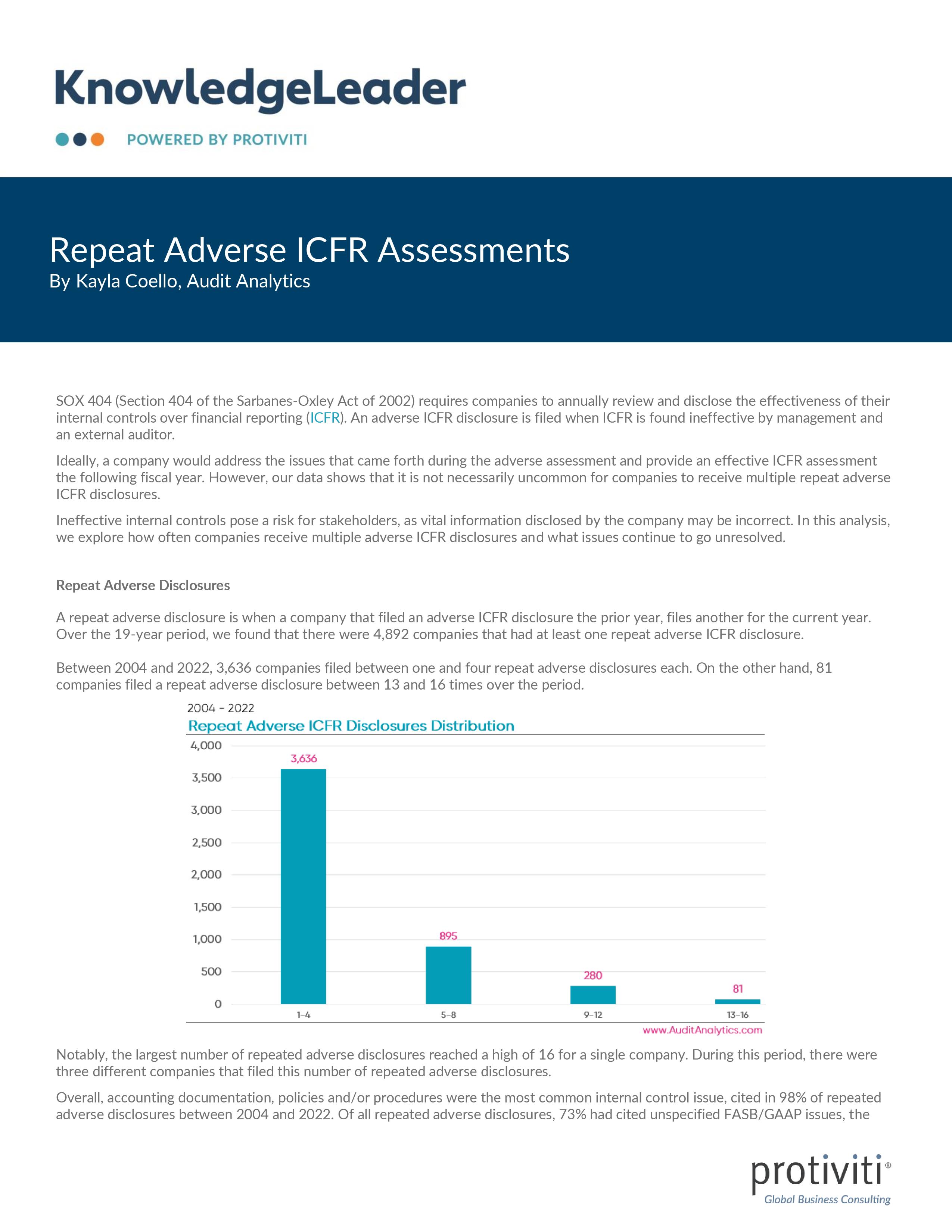

Section 404 of the Sarbanes-Oxley Act of 2002 requires companies to annually review and disclose the effectiveness of their internal controls over financial reporting (ICFR). An adverse ICFR disclosure is filed when ICFR is found to be ineffective by management and/or an external auditor. Ideally, a company would address the issues that came forth during the adverse assessment and provide an effective ICFR assessment the following fiscal year. However, data shows that it is not necessarily uncommon for companies to receive multiple repeat adverse ICFR disclosures.

In this analysis, Audit Analytics explores how often companies receive multiple adverse ICFR disclosures and what issues continue to go unresolved.