An SEC Sea Change? Proposed Amendments Could Reshape the Public Company Landscape

Actions Management and Boards Should Take Now

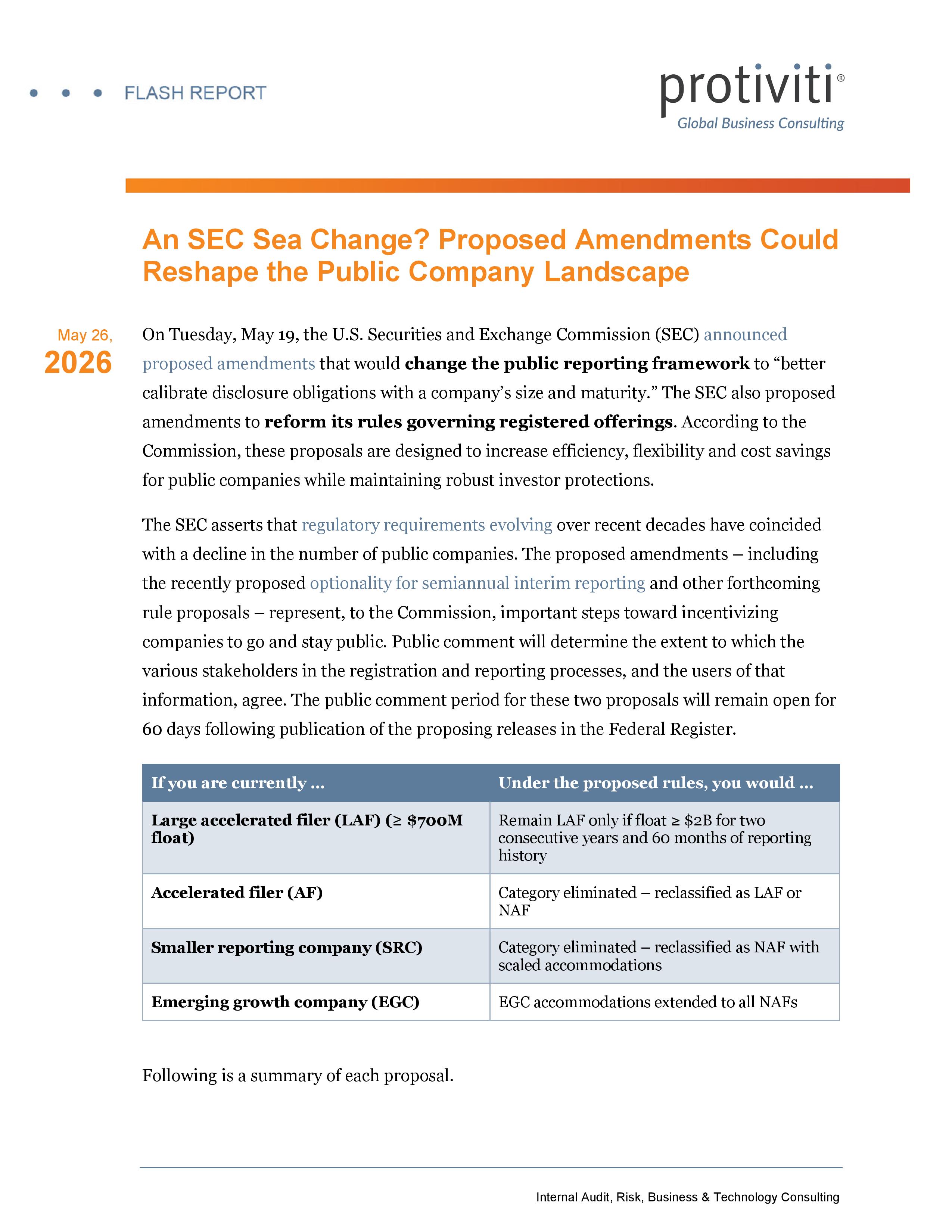

The U.S. Securities and Exchange Commission (SEC) has unveiled proposed amendments that promise to reshape the public reporting framework and transform how companies access capital markets. These changes aim to streamline classifications, reduce compliance costs, and encourage more businesses to go public. Key updates include the elimination of certain filer categories, such as accelerated filers and smaller reporting companies, expanded disclosure accommodations for smaller entities, and enhanced flexibility in registration and offering communications.

For corporate leaders, boards and legal professionals, understanding and adapting to these changes is critical. Despite faster processes and reduced administrative hurdles, diligence standards, liability exposure, and anti-fraud protections remain firmly intact. Organizations must prioritize assessing their reclassification status, leveraging expanded Form S-3 eligibility, and aligning internal controls with the evolving regulatory framework.

Key Takeaways:

- Simplified classifications and reduced compliance costs aim to make public markets more accessible without diminishing investor protections.

- Non-accelerated filers (NAFs) benefit significantly, including exemption from Section 404(b) auditor attestations.

- Diligence standards, liability exposure and anti-fraud safeguards remain unchanged, ensuring continued accountability.

- Companies should proactively evaluate their classification changes and align compliance strategies with the updated framework.